Retiree COLA

Retiree COLA

The retiree cost-of-living adjustment (COLA) is based on the average annual change in the U.S. Department of Labor, Bureau of Labor Statistics Consumer Price Index (CPI) for All Urban Consumers in the San Francisco-Oakland-Hayward area. According to the County Employees Retirement Law of 1937, the SCERS Board must determine the appropriate COLA for SCERS retirement benefits and implement that COLA on April 1st of each year.

In making the COLA calculation, the average annual CPI for the calendar year just ended is compared with the average annual CPI for the preceding calendar year and rounded to the nearest one-half percent. While the exact COLA amount will not be determined until the first quarter of the next calendar year, we have provided a COLA tracker to show retirees how the COLA is trending as of the most recent CPI data, which is released bimonthly. These values are estimates and subject to change with the next set of CPI data.

![]()

COLA adjustments for April 2024

COLA FAQs

The cost of living adjustment, or COLA, is a benefit that ensures your value of money at retirement keeps up with the rate of inflation.

After you retire, you may receive an annual COLA effectively in April of each year. Your COLA amount is unique to you and based on:

- The annual rate of inflation

- Your retirement tier

- The year you retire

Eligibility

Who is eligible?

SCERS has provided annual COLAs to retirees since the 1970s, under a structure authorized under state law and implemented by the Sacramento County Board of Supervisors.

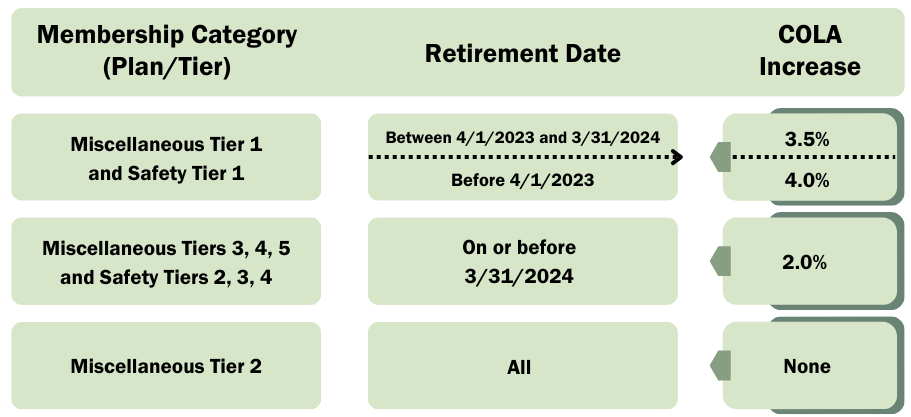

Miscellaneous Tier 1: up to 4%

Miscellaneous Tier 2: No COLA

Miscellaneous Tiers 3, 4, and 5: up to 2%

Safety Tier 1: up to 4%

Safety Tiers 2, 3, and 4: up to 2%

Consumer Price Index (CPI) Information

What makes up the CPI?

The COLA methodology is based on the changes in the Consumer Price Index for All Urban Consumers (CPI-U) for the region, as measured by the U.S. Department of Labor’s Bureau of Labor Statistics. The CPI-U represents an average of price changes that consumers pay for goods and services.

The CPI-U is one of many inflation measures. Another index is the CPI for Urban Wage Earners and Clerical Workers, or CPI-W. Federal law requires CPI-W to calculate Social Security benefits. California state law requires SCERS to use the CPI-U to calculate annual COLAs for retirement benefits.

CPI-U is a more general index and tracks retail prices more useful in reflecting the loss in purchasing power for retirees while CPI-W is geared more toward hourly workers. The CPI-W places a slightly higher weight on food, apparel, transportation, and other goods and services. It places a slightly lower weight than the CPI-U on housing, medical care, and recreation.

Please note that the CPI-U Bay Area index may not reflect your personal inflation experience or how you spend your money but is a statistical average of many households’ spending patterns. The measure provides a consistent, reliable, and valid method for SCERS to determine the COLA the same way every year. SCERS cannot pick a more favorable CPI index from year to year to influence a different outcome.

The Bureau of Labor Statistics updates the CPI-U for the Bay Area every two months. SCERS tracks how the COLA is trending here.

Where can I look for CPI data?

- Visit the US Bureau of Labor Statistics website here.

- Click on CPI Data (third blue box from the left, towards the top of the screen) and select Regional Resources. Select “San Francisco,” under Metro Areas on the right side of the screen.

SCERS uses the data points from the “annual” column to calculate the year-over-year change, and not the December-to-December data points. The “annual” data smooths out any spikes or dips that might occur during the year.

Please note that for CPIs that are only published every other month (such as for the San Francisco-Oakland-Hayward area), the BLS includes off-month CPI values that are not published in calculating the annual average. According to the BLS, “many food and energy prices are collected for the ‘off’ months, and the unpublished ’off-cycle’ indexes are interpolated and used in the annual average.”

As a result, a reader cannot reproduce the annual average shown in the table below because the off-month CPI values used by the BLS in their calculations are not available.

What is the formula?

As outlined in Government Code section 31870, SCERS uses the “percentage of annual increase or decrease in the cost of living as of January 1st of each year as shown by the current Bureau of Labor Statistics Consumer Price Index for All Urban Consumers for the area in which the county seat is situated.” Further, the amount is rounded “to the nearest one-half of 1 percent.”

SCERS has an established practice of using the Consumer Price Index for All Urban Consumers (CPI-U) for the San Francisco Bay Area region for the COLA process.

To determine the annual CPI increase, you must divide the annual CPI amount of the recent year by the annual CPI amount from the previous year.

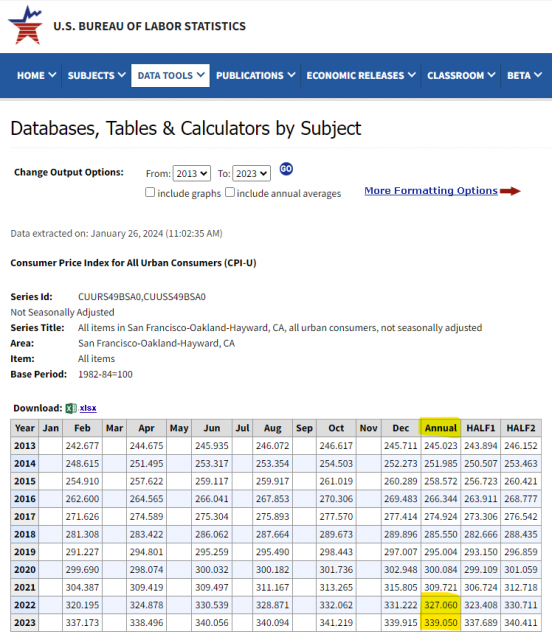

For example, for the COLA effective April 2024, the Bureau of Labor Statistics reports the annual CPI-U Bay Area for 2023 as 339.050 (1982-84 base year), and the annual CPI for 2022 as 327.060. Therefore, 339.050 (2023) divided by 327.060 (2022) is 1.0367, or an increase of 3.67%.

Or:

(339.050 – 327.060) / 327.060 = 3.67%

Rounded to the nearest one-half of 1 percent, the CPI that SCERS used for the April 2024 COLA was 3.5%.

COLA Bank

Is there a carryover in cost-of-living that exceeds the maximum COLA amount?

If a change in CPI indicates that inflation is greater than the maximum allowable COLA (for example, 2%), then the excess amount will be placed into what we call the COLA Bank.

If the COLA adjustment for a given year is going to be less than the maximum amount and the payee has a positive COLA Bank, SCERS will advance any available percentage to grant the payee the maximum COLA adjustment possible, up to the maximum amount (for example, up to 2%).

How does the COLA Bank work?

Let’s use the example of a SCERS retiree who is eligible to receive a 2% maximum COLA each year.

If CPI shows a 3% increase, the maximum of a 2% adjustment can be applied to the payee’s benefit, and the remaining 1% would go into the COLA Bank.

If the CPI for a given year shows less than a 2% increase, and the payee has a positive COLA Bank, SCERS will advance any available percentage to grant the payee the maximum COLA adjustment possible up to the full 2%.

Through the 2010s, the U.S. experienced historically low inflation. As a result, many Tier 1 members with a maximum 4% COLA received higher COLAs than the rate of inflation because of the COLA Bank.

How much is my COLA Bank?

See tables below:

Miscellaneous Tier 1 and Safety Tier 1

|

Retirement Date |

Accumulated Bank as of April 1, 2024 |

|

Before 7/1/1967 |

26.0% |

|

7/1/1967-6/30/1968 |

25.5% |

|

7/1/1968-3/31/1969 |

24.5% |

|

4/1/1969-3/31/1970 |

22.0% |

|

4/1/1970-3/31/1971 |

19.5% |

|

4/1/1971-3/31/1972 |

17.5% |

|

4/1/1972-3/31/1973 |

16.5% |

|

4/1/1973-3/31/1974 |

16.0% |

|

4/1/1974-3/31/1975 |

13.0% |

|

4/1/1975-3/31/1976 |

6.0% |

|

4/1/1976-3/31/2023 |

1.0% |

|

4/1/2023-3/31/2024 |

0.0% |

Miscellaneous Tiers 3, 4, 5 and Safety Tiers 2, 3 and 4

|

Retirement Date |

Accumulated Bank as of April 1, 2024 |

|

Before 4/1/1997 |

24.5% |

|

4/1/1997-3/31/1998 |

24.0% |

|

4/1/1998-3/31/1999 |

22.5% |

|

4/1/1999-3/31/2000 |

21.5% |

|

4/1/2000-3/31/2001 |

19.5% |

|

4/1/2001-3/31/2002 |

17.0% |

|

4/1/2002-3/31/2007 |

15.0% |

|

4/1/2007-3/31/2008 |

14.0% |

|

4/1/2008-3/31/2012 |

13.5% |

|

4/1/2012-3/31/2013 |

13.0% |

|

4/1/2013-3/31/2015 |

12.5% |

|

4/1/2015-3/31/2016 |

11.5% |

|

4/1/2016-3/31/2017 |

11.0% |

|

4/1/2017-3/31/2018 |

10.0% |

|

4/1/2018-3/31/2019 |

9.0% |

|

4/1/2019-3/31/2020 |

7.0% |

|

4/1/2020-3/31/2022 |

6.0% |

|

4/1/2022-3/31/2023 |

5.0% |

|

04/1/2023-3/31/2024 |

1.5% |

Prior Year COLA Information

| Date | Membership Category (Plan/Tier) | Retirement Dates | COLA Increase |

|---|---|---|---|

| April 1, 2023 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/2022 |

4.00% |

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

On or before 3/31/2022 |

2.00% |

|

| April 1, 2022 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1976 |

4.00% |

|

From 4/1/1976 to 3/31/2022 |

3.00% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

On or before 3/31/2022 |

2.00% |

|

| April 1, 2021 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1977 |

4.00% |

|

From 4/1/1977 to 3/31/1978 |

2.50% |

||

|

On or after 4/1/1978 |

1.50% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

On or before 3/31/2020 |

2.00% |

|

|

On or after 4/1/2020 |

1.50% |

||

| April 1, 2020 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1978 |

4.00% |

|

On or after 4/1/1978 |

3.50% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2019 |

Miscellaneous Tier 1 and Safety Tier 1 |

All |

4.00% |

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2018 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1978 |

4.00% |

|

On or after 4/1/1978 |

3.00% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2017 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1978 |

4.00% |

|

On or after 4/1/1978 |

3.00% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2016 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1979 |

4.00% |

|

On or after 4/1/1979 |

2.50% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2015 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1979 |

4.00% |

|

On or after 4/1/1979 |

3.00% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2014 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1979 |

4.00% |

|

On or after 4/1/1979 |

2.00% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2013 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1979 |

4.00% |

|

From 4/1/1979 to 3/31/1980 |

3.00% |

||

|

On or after 4/1/1980 |

2.50% |

||

|

Miscellaneous Tiers 3, 4, and 5 and Safety Tiers 2, 3, and 4 |

All |

2.00% |

|

| April 1, 2012 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1980 |

4.00% |

|

On or after 4/01/1980 |

2.50% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

All |

2.00% |

|

| April 1, 2011 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1980 |

4.00% |

|

On or after 4/01/1980 |

1.50% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

On or before 3/31/2008 |

2.00% |

|

|

On or after 4/01/2008 |

1.50% |

||

| April 1, 2010 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1981 |

4.00% |

|

On or after 4/01/1981 |

0.50% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

On or before 3/31/2008 |

2.00% |

|

|

From 4/01/2008 to 3/31/2009 |

1.50% |

||

|

From 4/01/2009 to 3/31/2010 |

0.50% |

||

| April 1, 2009 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1981 |

4.00% |

|

On or after 4/01/1981 |

3.00% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

All |

2.00% |

|

| April 1, 2008 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1981 |

4.00% |

|

On or after 4/01/1981 |

3.50% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

All |

2.00% |

|

| April 1, 2007 |

Miscellaneous Tier 1 and Safety Tier 1 |

On or before 3/31/1981 |

4.00% |

|

On or after 4/01/1981 |

3.00% |

||

|

Miscellaneous Tier 3 and Safety Tier 2 |

All |

2.00% |

Other FAQs

Is there a flat rate or a minimum?

No. The COLA provision amounts compound annually and isn’t based on a flat rate each year or a minimum.

How can I see how much my COLA is worth?

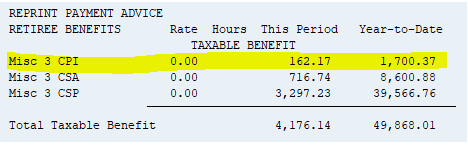

The cumulative COLA payment since retirement is displayed on your monthly pay advice, as part of the CPI line (see example).

The annual change in COLA amount will be reflected when comparing the March payment to the April payment.

Example:

Please note that SCERS has discontinued mailing individual notices to retirees because the same information is available on the monthly pay advice.

What is the Board of Retirement’s role?

Each year, usually in February, the SCERS Board of Retirement approves the COLA amounts using a formula established by California law. This is an administrative role; the Board does not have the discretion to determine COLA levels outside of the law.